Last updated:

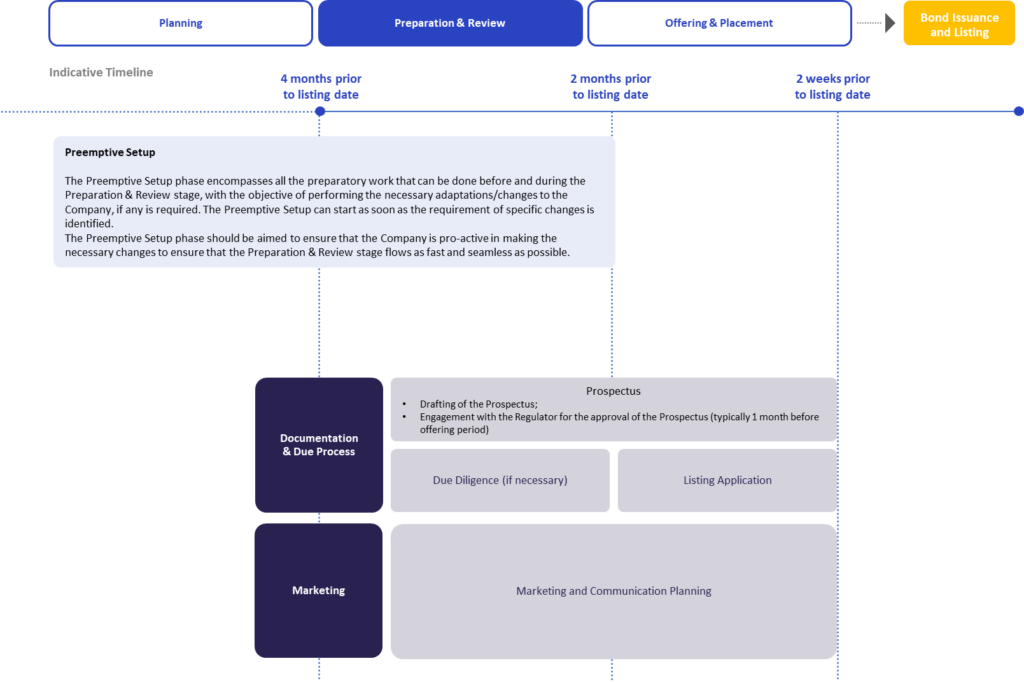

The preparation phase may take between 2 to 4 months before finalizing the process of admitting the bonds to trading. The preparation phase (as the planning phase) will vary greatly dependent on several factors such as: the Company´s development stage, if it is the first issuance or not, if you have a base Prospectus, if the Company will launch a public or private offer and if you chose a regulated market or an MTF for listing.

What are the necessary preparation steps you need to take?

4.1.1.2.1. Preemptive setup

4.1.1.2.1.1. Kick-off meeting

Once all members of the Bond Offering team have been selected, the kick-off meeting brings them together to agree on:

4.1.1.2.1.2. Adapt corporate governance structure and internal compliance functions

How efficient, compliant and accountable is your Company?

Corporate Governance structure

Companies that intend to have bonds admitted to trading on Regulated Markets may have to adapt their Corporate Governance structure. Below it is presented the obligations that these companies must fulfill in what regards their organizational structure:

*To be independent, the members must not be associated with any specific interest group of the Company or be under any circumstances likely to affect their exemption from analysis or decision. Particularly, to assure their independence, members cannot (i) hold or act on behalf of holders of a holding equal to or greater than 2% of the Company’s share capital; and (ii) have been re-elected for more than two terms, continuously or interspersed.

Review of internal functioning and organisation

Your Company should also anticipate the rules applicable to companies with bonds listed in order to allocate the necessary resources and put in place the internal compliance functions, processes and systems necessary to guarantee the compliance with those rules.

Recommended reading: 5. Life as a Company with securities admitted to trading.

4.1.1.2.1.3. Adapt financial accounts, if necessary

Depending on the market your Company wishes to list its bonds, different rules on accounting standards apply.

For example, a Company with bonds admitted to trading on a Regulated Market, such as Euronext Lisbon, is required to report financial accounts in compliance with the international accounting standards accepted at European level, corresponding to IAS/IFRS or accounting standards considered equivalent to IFRS by the European Commission.

The Company will therefore have to consider the requirements related to adoption of these accounting standards. You might require assistance from certified accountants in order to fully understand the impact of change in the accounting framework (although the recent trend has been a gradual convergence between standards). Nevertheless, although IFRS can be more complex, it presents the advantage of comparability with companies at European level, which may promote the Company notoriety towards international and Institutional Investors. Hence, if you need to convert your accounts you can easily be assisted by a professional and this conversion will enable you to benefit from the advantages stated.

A Company with bonds admitted to trading on Euronext Growth and Euronext Access has the choice of reporting its accounts in accordance with IFRS, or accounting standards considered equivalent to IFRS by the European Commission, or with the accounting standards applicable in Portugal (i.e. SNC).

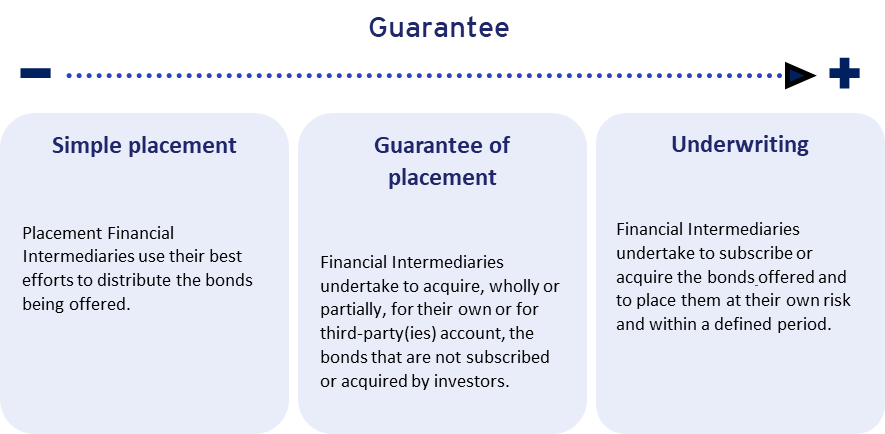

4.1.1.2.1.4. PLACEMENT agreements and appointment of Placement Financial Intermediaries

At the beginning of the Bond Offering journey the Company’s management meets with potential Bond Offering partners that may be appointed to support the Bond Offering process, as well as the Company on the life after becoming a company with listed bonds.

Moreover, your Company may appoint one or more Placement Financial Intermediaries that will be in charge for the distribution of the offered bonds and will negotiate and enter with such Placement Financial Intermediary(ies) a placement agreement to regulate the terms and conditions of the distribution services.

The negotiation of a placement agreement may require some time and should start early in the bond offering preparation phase. Signing must occur prior to the approval of the Prospectus by the Regulator.

4.1.1.2.1.5. Internal decision-making process

The decision to offering bonds to the public and related decisions during the bond offering journey require the prior approval of corporate resolutions during the Preparation phase, such as:

The general meeting of the Company is responsible for approval of the decision to issue bonds, except if its articles of association empower the board of directors with such competence. In any case, the resolution approving the bonds issue typically delegates power to the board of directors or managers to take decisions during the preparation process.

4.1.1.2.1.6. Engagement with the Regulator, the Stock Exchange and the Central Securities Depository

The applications for the Prospectus approval by the Regulator (in Portugal, the CMVM), for the listing approval by the Stock Market Operator (in Portugal, Euronext Lisbon) as well as for the registration of the Company’s bonds with the Central Securities Depository (in Portugal, Euronext Securities Porto) should be filed with a set of legal and financial documents set out in the applicable laws and regulations.

It is recommended that the Company, and its advisors, engage with these entities in an early stage of the Bond Offering journey for a smooth and timely approval procedure.

4.1.1.2.2. Due Diligence

Contrary to what occurs in equity offerings, in bond offerings the due diligence will normally only take place in case there is either an underwriting of bonds by the arrangers or some sort of offering / roadshow to institutional investors, normally at the request of the underwriters or these investors. Furthermore, since bond offerings do not entail a change of the issuer’s shareholding structure, the scope of this due diligence is usually more restricted than equity offerings’ due diligences, including only financial, commercial, legal, accounting and tax matters that may be deemed key by the underwriters or institutional investors.

This process is intended to provide knowledge of the Company, allowing it to correct any issue before the offering of its bonds and supporting it with strengthening of its business and corporate governance practices as well as ensuring that the required information about the Company will be disclosed in the Prospectus. Throughout the Bond Offering process, additional due diligence sessions may be planned at each key milestone to ensure that the information disclosed is up to date.

Recommended reading: 4.1.1.2.3. Prospectus.

Why should a Due Diligence be performed in the context of a Bond Offering?

The purpose of conducting a Due Diligence process in the context of a Bond Offering may be to:

As a best practice all information included in the Prospectus should be tied to a source document that was duly analysed during the Due Diligence and confirmed by the Company’s board, management of the Company and its external advisers (legal, accounting and any others as appropriate).

4.1.1.2.3. Prospectus

If you decide to proceed with a Public Offering in which the offer size and/or structure does not meet one of the exemptions presented in section ‘4.0. Road to Debt offering’ and/or you will request admission of the offered bonds to a Regulated Market, you will have to prepare and disclose to the public a Prospectus approved by the Regulator, drafted in accordance with the EU Prospectus Regulation.

What is the Prospectus?

The Prospectus is a legal document, which provides to potential investors and analysts all material key information that may affect the investment decision. The Prospectus includes legal, financial (both historical and prospective financial information) and commercial information with contents adapted to the Company’s profile and bonds.

This document enables investors to clearly assess the Company’s patrimony, financial situation, results, and prospects. The Prospectus must be complete, understandable, and consistent. Once approved by the Regulator, it will be published prior to the bond offering or admission to trading.

The Prospectus may be drafted as a single document or as separate documents, dividing the required information into:

Summary*

The summary should be drawn up in a standardised format and in a concise manner, using simple language to make it easier to understand.

The summary should contain i) key information regarding the risks of the Issuer and the bonds that are being offered, ii) the offer’s terms and conditions, and the reasons for the offer and the allocation of revenues.

*The summary may not be required.

Registration Document

Document presenting the Issuer, its sector and business activities, including risk factors, assets and liabilities, accounting and financial information, management, and corporate governance, among others. It contains the information that will subsequently be shared with investors and analysts through the media, ensuring fair and equal diffusion to all parties.

Securities Note

Document defining the main terms of the transaction and information on the bonds that are being offered and / or intended to be admitted to trading, including the number of bonds, the distribution price, the relative seniority of the bonds in the Company’s capital structure, the interest rate and maturity date, a calendar for the offer, and the use of proceeds.

What is an EU Growth Prospectus?

Considering the specificities of the different types of bonds, Companies, offers and admissions, the EU Prospectus Regulation foresees different types of Prospectus, such as the EU Growth Prospectus. This is a simplified Prospectus for certain Companies, with limited page numbers and less information required, making it easier for these companies to access the capital markets. The EU Growth Prospectus may be used regardless of the market segment in which the issuance will take place.

In what context can a company choose to draw up an EU Growth Prospectus?

Companies which comply with the guidelines below can opt for the simplified EU Growth Prospectus, provided that they do not have securities admitted to trading on a Regulated Market:

► Companies, classified as SMEs, i.e. according to their last annual or consolidated accounts, they meet at least two of the following three criteria:

· an average number of employees under 250;

· total assets recorded in the Balance Sheet do not exceed €43m;

· annual net turnover does not exceed €50m.

► Companies, other than SMEs, whose securities are traded or are to be traded on an SME growth market, provided that those Companies had an average market capitalisation of less than €500m on the basis of end-year quotes for the three calendar years prior.

► Companies, other than the ones mentioned above, where the offer of securities to the public does not exceed €20m calculated over a period of 12 months, and provided that such companies have no securities traded on an MTF and have an average number of employees during the previous financial year which does not exceed 499.

What is EU passporting of Prospectus?

As EU Prospectus rules are similar in all Member States, once a Prospectus has been approved in one EU country, it is valid throughout the EU (through the passport mechanism). This represents an important simplification for Companies since allows Companies to launch offers or admit to trading debt instruments in several EU countries, resorting to the same Prospectus, provided that the Company requests the Regulator approving the Prospectus to send it (passport) to the Regulators of the relevant Member States.

What is CMVM approach?

CMVM recognizes that streamlining the conditions for issuers to access financing through capital markets, together with ensuring high quality standards for information to be provided to investors, generates trust and is a key element for the development of the Portuguese capital markets.

In the context of public offers or admission to trading processes, CMVM assumes as a priority the commitment with specific approval dates and the agility in reaction times to analyse Prospectus and recognizes the importance of calendars’ predictability as essential conditions for a smooth Prospectus approval processes.

Predictability & Timeline

– Interactions and approval according to a calendar previously agreed with the Issuer;

– Clear comments and understandings (in writing) – focus on the crucial information for investors;

– Quick reactions to drafts (commitment and track record [link]).

CMVM assumes the Issuer´s commitment to complete reactions, for the benefit of the procedure.

Availability & Agility

– Kick off meeting (if requested) before preparing and submit the Prospectus and further meeting (as needed);

– Credible and responsive process, coupled with smooth and informal interactions during all the process.

Prospectus process

The Prospectus must include complete, true, updated, clear, objective and lawful information regarding, for example:

CMVM will be available to clarify any queries during the drafting procedure.

What information needs to be included in the Prospectus?

Business Description

The Prospectus provides a brief history of the business and a timeline of key-events of the company across time. It also contains details about the Company’s incorporation and an explanation of the Company’s strategy.

The Company’s core economic operations are also described in the Prospectus, informing potential investors about the goods and services it offers as well as any recent changes to its business model.

Risk Factors

The Prospectus must disclose all material risk factors that may affect the Issuer and its bonds. If a Due Diligence process takes place, risk factors may be identified during such process.

Issuer’s financial data

The Prospectus must include the Annual Accounts for the last two financial years (or such shorter period as the Company has been in operation).

All historical financial information must be audited and certified by a Charted Accountant. Additionally, in case there is a material change (usually a transaction), additional financial information may need to be disclosed, namely, on how that event affected the financial position of the Company.

Deal Structure

A description of the offer must be included in the Prospectus, allowing investors to understand the characteristics of the offer and features of the bonds (including the rights attributed to bondholders).

Credit ratings

It must be disclosed, if applicable, credit ratings assigned to the bonds at the request or with the cooperation of the issuer in the rating process and a brief explanation of the meaning of the ratings if this has previously been published by the rating provider.

Profit forecast

Although not mandatory, it may be recommended (or, in certain cases, if already disclosed, it may be mandatory) to include in the Prospectus, as this is relevant information for investors, prospective financial information in the form of a financial performance forecast.

Tax information

The Prospectus must include a warning that the tax laws of the investor’s Member State and the Issuer’s Member State of incorporation may affect the income received on the bonds.

Additionally, the Prospectus shall include proper information in the case that the proposed investment originates a special tax regime, as for example in the case of investments in bonds which give investors favourable tax treatment.

Offer price and intended use of proceeds

It is allowed not to mention, in the Prospectus, the final offer price and/or the final number of bonds offered to the public, provided that:

· The Prospectus discloses the criteria, and/or the conditions applicable in the determining the offer price and quantity of bonds or, the maximum price and amount of shares to be offered; or

· Acquisitions or subscriptions may be withdrawn for a period of no less than three working days following disclosure of the final offer price and the amount of bonds offered.

As soon as the final offer price and the final number of bonds offered are determined, they must be notified to the CMVM and disclosed.

As the Company will often offer an issue of securities when it is unable to raise capital internally to finance a large investment (e.g. expand its operations to other geographical locations, acquire proprietary technology, production of a new line of products), the Prospectus should include some considerations about the intended use of the proceeds of the operation.

Language

Public offers’ Prospectuses in Portugal are generally drafted in Portuguese, although it is very common to be drafted in English, with a Portuguese version of the Summary, if necessary.

Companies should meet, early in the process, with the Regulator to present the main features of the offering and to agree on an indicative timetable for the Prospectus approval procedure. These interactions are extremely important for a smooth procedure and to agree on the calendar for the versions of the draft Prospectus to be submitted to the CMVM as explained above in “What is CMVM approach?”

What is the timing for the Prospectus approval?

Preliminary calendars are usually agreed upon with the CMVM so that the Company has some idea of when it can expect the competent authority to ratify the Prospectus.

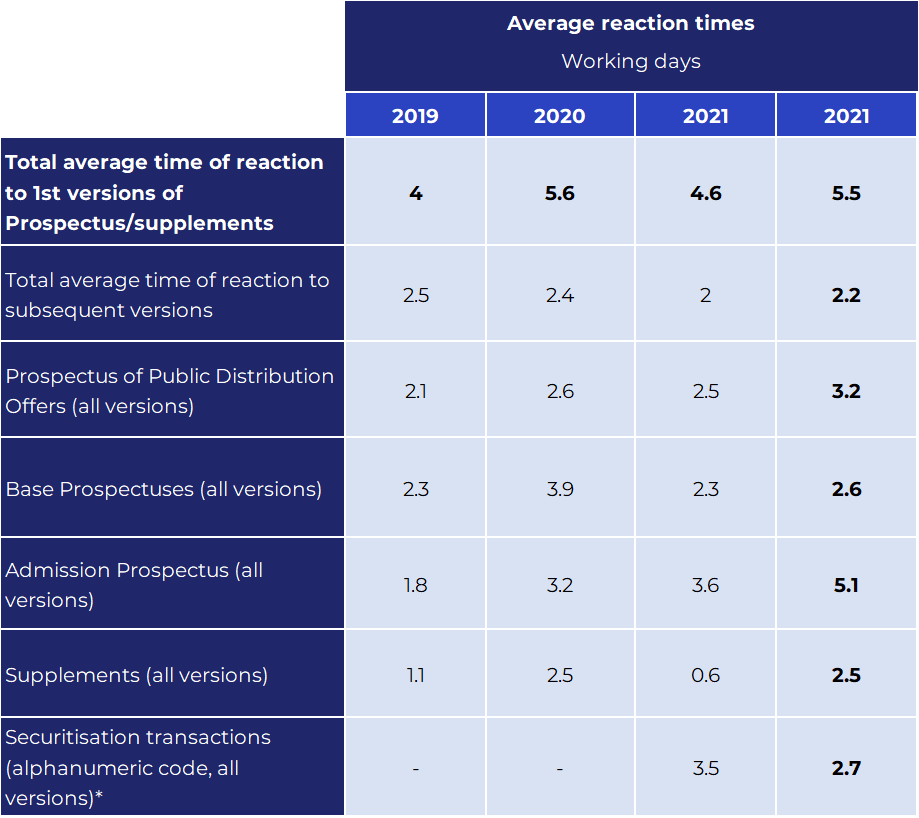

CMVM has disclosed and will periodically continue to disclose the timeline of its reactions in the context of prospectus approval procedures, aligned with its public commitment with fast, predictable, and transparent procedure, ensuring that the revision process takes into account the companies financing needs and market opportunities.

Below you can find data on the average timeline for CMVM reaction to the multiple versions of Prospectus supplements and securitization transactions:

*Monitoring began in 2021. In 2022, the CMVM authorised more than 28 titularisation operations, involving more than €1 billion of bonds issued.

The CMVM conducts a thorough review to verify the adequacy of the Prospectus with the legal requirements relating to its content and form, particularly by examining the completeness, comprehensibility and consistency of the content, and to ensure that the Prospectus contains all the information needed for investors to make an informed decision.

This review period starts when a first draft of the Prospectus is filed with the Regulator. Afterwards, through an interactive and streamlined process, the Prospectus is revised and a final version is submitted for CMVM’s approval, in accordance with the calendar and the Company’s needs.

The approval of the Prospectus implies a verification of the completeness, consistency and comprehensibility of the information Included in the Prospectus. The CMVM will ensure that all the information contained in the Prospectus meets the minimum requirements for investors to be able to make informed decisions about the bonds.

Once the CMVM grants approval, the Prospectus is published on CMVM’s website. All approved Prospects are published on CMVM’s website, which provide examples prior to start drafting the Company’s Prospectus.

Once approved, the Prospectus must be made available to the public at a reasonable time in advance of, and at the latest at the beginning of, the offer to the public or the admission to trading of the bonds involved. Click on the button below to find out where the Prospectus must be published.

Where must the Prospectus be published?

The Prospectus must be made available to the public in electronic form on any of the following websites:

a) the website of the Issuer, the offeror or the person asking for admission to trading;

b) the website of the Placement Financial Intermediaries placing or selling the bonds, including paying agents;

c) the website of the Stock Market Operator where the admission to trading is pursued;

d) the website of the Regulator who as approved the Prospectus.

The Prospectus must be published on a dedicated section of the website which is easily accessible when entering the website. It must be downloadable, printable and in searchable electronic format that cannot be modified.

Validity

The Prospectus for a Public Offering for distribution remains valid for a 12-month period from the date of their approval by the CMVM, and provided the Prospectus is updated accordingly with any supplements that may be required. In particular, a base Prospectus might be a relevant and very interesting tool providing companies with sufficient flexibility to fulfill emerging financing needs throughout a period of 12 months after its approval.

Supplements

It may occur that in the time between the approval of the Prospectus and the time when trading on a Regulated Market begins a material mistake or a material inaccuracy relating to the information included in a Prospectus, which may affect the valuation of the bonds.

In these cases, the Company must issue a supplement to the Prospectus with the relevant information and request approval of the document from CMVM. The supplement approval process takes into account the fact that it arises at the specific time where CMVM’s fast reaction is off upmost importance to mitigate the potential disruption of such event. Therefore, supplements are approved very quickly after the emergence of a triggering event, allowing investors who have already presented subscription orders the right to withdraw them.

Investors who accepted the offer prior to the disclosure of the supplement have the right to withdraw their acceptance within not less than three working days following the disclosure of the supplement, provided that the significant new factor, material mistake or material inaccuracy arose or was noted before the closing of the offer period. That period may be extended by the Company or the Offeror. The final date to exercise the right of withdrawal must be stated in the supplement.

4.1.1.2.4. Listing application

In order for a Company’s bonds to be admitted to trading, a request for the listing of the bonds must be submitted to the stock market operator. In Portugal the operator is Euronext Lisbon, who will verify compliance with the general requirements for admission to trading.

Recommended reading: 3.1.1.1.2. Eligibility criteria.

In case of listing in Portuguese markets, to kick-off the admission to trading process, the Company first meets with Euronext to present the listing project and agree on a timetable regarding the admission to trading process.

The Company must appoint a Listing Agent (Euronext Lisbon) and a Listing Sponsor (Euronext Growth and Euronext Access) who will assist and guide the Company with the admission to trading and also help the Company to prepare the application form and all the documentation that must be submitted to Euronext Lisbon.

At the same time as the proceedings above, the Company needs to register its bonds with the Portuguese Centralised System of Registration of Securities managed by Euronext Securities Porto.

Decision

Euronext will decide on the application for admission to listing within a maximum period of 30 trading days (1 month for Euronext Growth and Euronext Access) after receiving the required documentation, unless agreed otherwise by the applicant Company and Euronext Lisbon.

In the event of a Public Offering of bonds, the admission to trading shall become effective only after the assessment of results and settlement of the offering.

4.1.1.2.5. Marketing and Communication Planning

Marketing and Communication strategy throughout the Bond Offering process is crucial as it enables the Company to manage investor relations; generate interest and mitigate perceived uncertainty.

In the context of a Bond Offering, it is of paramount importance that the Company, with the assistance of its advisors, diligently defines how to present and promote the offer to potential investors.

While the Prospectus is being drafted, a marketing strategy is designed to create investor interest and momentum. The Company and its advisors may draw up a presentation to use in meetings with investors, which includes exclusively contents presented in the Prospectus.

Marketing documents may be prepared, according to the type of offering, such as slideshow, dedicated websites, press releases and other communication materials, which may all be adjusted throughout the Bond Offering process.. Documents comprising advertising content are subject to prior approval by the CMVM.

The marketing strategy has a great impact in managing investor relations, generating interest and mitigating perceived uncertainty.

It should be highlighted that material information provided, directly or indirectly, by the Company to Institutional Investors or special categories of investors, including information disseminated at meetings, as well as information provided to financial analysts shall be disclosed to all investors to whom the offer is addressed.

Until the offer is made public, all the parties involved in its preparation need to:

As from the moment the offer is made public, all the parties involved in releasing information regarding the offer need to:

Additionally, when conducting pre-offering marketing activities, such as the ones described above, all the parties involved in the Offer need to assure the compliance with the EU Market Abuse Regulation (“MAR”) in what respects disclosure of inside information the context of a market sounding.

Recommended reading: 5. Life as a Company with securities admitted to trading.

4.1.1.2.6. Early-look meetings with investors

The targeting of investors in debt offerings is not exactly the same as in an equity offerings. Whereas in the latter it is more common to have an offering to institutional investors (in parallel with the Public Offering) that plays a key role in the process and the success of an IPO, notably in the price determination thought the bookbuilding method, the role of these investors is much more limited in debt issuances.

This is without regards that the investors may be consulted, at an early stage, to assess and attract their interest in the issuer and bond issuance and, thus, help set the offer price.

Considering the offer structure, it may be advisable to prepare the Company’s Management for any meetings with potential investors (either internally or through a communication agency or other advisors) in order to create adhesion by investors.

These one-on-one confidential early-look meetings between Management and targeted investors aim to introduce the Company, explain its business model, assess the initial market sentiment on the Company’s story, ask for the investors’ feedback on several matters, such as the Bond Offering and the bond price, to understand how the market will assess and value the Company.

These early-look meetings may allow an early assessment of the potential success of the Bond Offering. Based on the potential interest noticed at these meetings, which may be spread out over time, the Company may adjust its Bond Offering project, and can postpone or even exit the process without a substantial financial commitment at this stage.

If the meetings generate a formal commitment of acceptance of the Offer, this information will appear in the Prospectus.